Net present value (NPV) tells us the potential value of an investment by calculating the difference between the net present value of cash inflows and the net present value of cash outflows over a specific time period. In simple words, NPV helps an investor predict if they can achieve their target yield from a prospective investment opportunity, by calculating the total value of an investment opportunity by discounting all the future inflows and outflows of cash to the present day.

Some Important points to note:

NPV takes into consideration the time value of money and helps you calculate the present value of all cash inflows and outflows in the future.

If the NPV of a project is positive, it simply means a positive return on your investment, thereby making the prospective project more attractive for investors. However, if a project has a negative NPV, it needs to be avoided.

In order to calculate the NPV, one needs to accurately estimate the future cash flows and also come up with the correct discounted rate, as these are important to access the profitability of a project.

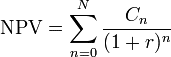

Net Present Value Formula :

Where,

Cn = Stands for cash flows during a period (n)

r = Stands for the discounted rate of return

n = Stands for the time period, and

N = Stands for holding period

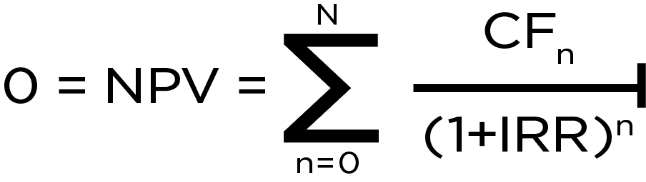

IRR is a financial metric that helps one calculate the profitability of future investments. For the calculation of IRR, the NPV of an investment is set at “zero”. In simple words, IRR is the percentage of money earned on an investment, just like the interest that one receives on a fixed deposit in a bank. IRR gives the investor a tool to compare the investment opportunities based on the yields they can produce.

Here are some key points that one must remember when calculating IRR:

- The calculation of IRR does not take into consideration external factors like inflation, financial risk, cost of capital or risk-free rate.

- IRR calculates the annual growth that a business can generate. It is ideal for comparing the projects based on their returns over time.

Let us now take a look at the IRR formula:

Leave a Reply