In order to find the inflationary gap, calculating GDP is necessary as it helps find real GDP.

As per its definition, “GDP measures the monetary value of final goods and services—that is, those that are bought by the final user—produced in a country in a given period of time”. While GDP is an important factor in knowing the economic condition of a nation, it accounts for the current time only and does not include inflation. To account for inflation in GDP, we require Real GDP.

Below are the formulas needed to calculate GDP and Real GDP.

GDP = Y = C + I + G + NX

Whereas:

- Y = Nominal GDP

- C = Consumption expenditure

- I = Investment

- G = Government expenditure

- NX = Net exports

Once we receive GDP, we can calculate Real GDP as:

Real GDP = Nominal GDP (Y) / D

Whereas D = GDP deflator (changes in prices of goods and services)

The difference between GDP and Real GDP is the fact that real GDP also considers inflation to reflect the changes in the price levels to provide a more realistic picture of the economic condition of a country.

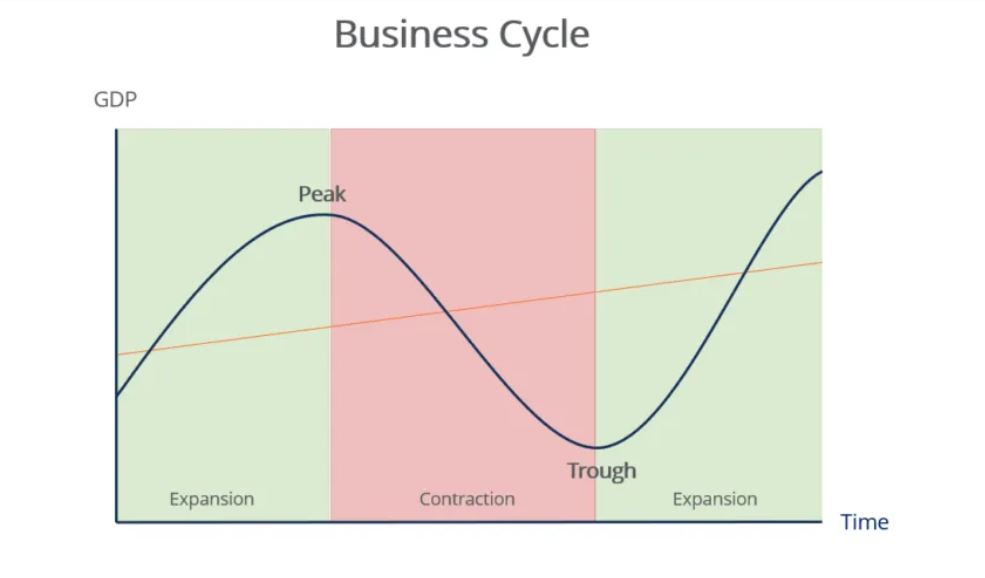

Impact of the inflationary gap on business life cycle

As promised, here is how the inflationary gap impacts an economy’s business life cycle.

A business cycle represents the periods of expansion and contraction in an economy. It has six phases: Expansion, peak, recession, contraction, depression, trough, and recovery. Each of these phases has a different impact on economic factors such as income, employment, profits, demand and supply, investments, and overall economic output.

Coming back to the inflationary gap, in the business cycle, it occurs when the expansion phase is taking place. When Real GDP goes higher than the expected GDP, it leads to more people having jobs with better pay scales.

As the purchasing power of people increases, their demands for goods and services accelerate, and that increases inflation, leading to an inflationary gap. The outcome is that the business cycle reaches its peak with the maximum possible growth and price levels. To combat soaring prices of goods and services, the government intervenes with measures which result in a period of recession followed by contraction, which has higher unemployment rates and lower economic output.

Thus, it can be said that the inflationary gap and the business cycle of an economy are highly related.

What does the inflationary gap mean in economics?

Till now, we discussed the inflationary gap in layman’s terms. Let’s understand it now as a concept of economy.

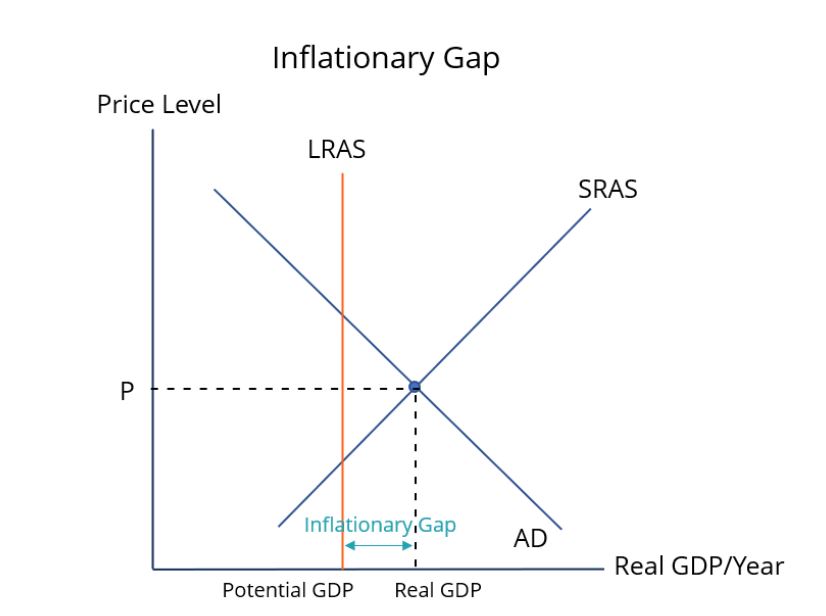

Whereas,

LRAS: Long-run Aggregate Supply

SRAS: Short-run Aggregate Supply

AG: Aggregate Demand

-> As seen in the chart, in the short period, the aggregate supply increases as the inflationary gap rises because businesses try to maximise their profit by providing more goods and services to benefit from the price hike. Thus, the SLRS line has an upward slope. However, this situation does not persist in the long run.

-> In the long run, the supply becomes dependent on the available resources in the country, which is limited. As a result, LRAS is a vertical line.

-> We can see that the Real GDP is the intersection of AG and SRAS. The difference between that intersection and potential GDP shown in the graph is the inflationary gap.

This is also related to the business cycle discussed above. Once an inflationary gap rises and reaches a peak, it results in contraction.

Measures to control the inflationary gap

While the inflationary gap is associated with full employment, a persistent situation results only in higher prices and worsens the economic condition of people. In order to control it, the government generally implements measures via monetary and fiscal policies.

- Monetary policy: Typically, central banks make decisions on monetary policy and increase the interest rate to control the supply of money in the market. As interest rates increase, banks raise their interest for lending money, too. This results in people having less money to spend, and inflation eventually comes under control.

- Fiscal policy: Governments make decisions on fiscal policy. The aim of this policy is also to control the supply of money. However, this is done by increasing taxes and reducing government expenditure.

These measures help the government to have control over their money supply and control the levels of inflation. In India, the Reserve Bank of India is responsible for undertaking tasks related to monetary policy and deciding on interest rates.

The bottom line

The inflationary gap is the difference between Real GDP and potential GDP. It increases employment in a country leading to higher purchasing power. The inflationary gap has a direct impact on the economic condition of a nation as it affects how businesses perform and people spend their money. While in the short run, the inflationary gap increases the prices of goods and services, the situation loses its momentum in the long run when the government intervenes with measures such as a fiscal and monetary policy to control the money supply.